Financial market investing has the potential to yield positive returns, but it is not without its share of difficulties, risks, and complexities. Taxes are a common obstacle that investors must overcome.

A number of incentives and credits exist to help small businesses make long-term investments. An example of such a relief is the “Investors’ Relief,” which is intended to provide favourable tax treatment to investors in certain types of companies.

This article will examine Investors’ Relief in depth, explaining what it is and discussing its eligibility requirements, benefits, and some caveats.

Understanding Investors’ Relief

Investors’ Relief is a tax advantage aimed at individuals who sell qualifying shares in a trading company or its holding company. This relief mirrors the trading company definition discussed earlier in relation to BADR.

When you claim Investors’ Relief, the profits from these shares are taxed at a favourable 10% rate. Additionally, when calculating taxes on other gains, like those from property sales, the 10% taxed gains from Investors’ Relief are given priority in utilising any remaining basic rate allowance.

Importantly, gains eligible for this relief are capped at £10 million per person over their lifetime, providing a significant tax advantage. This limit is separate from the cap that applies to BADR.

Gains Eligible for Relief

When a person sells shares in a trading company that is not on a stock exchange, the shares may have been bought at different times and in different ways.

Some shares could have been bought and kept for at least three years, making them ‘qualifying shares.’

Other shares may have been bought, but they haven’t been held for three years yet. These shares are called “potentially qualifying shares,” and they are still eligible for the tax relief.

“Excluded shares” are shares that were not bought through subscription but were bought from another shareholder (other than a spouse). “Excluded shares” do not qualify for relief.

Only the part of a capital gain from selling shares that comes from qualifying shares will qualify for investors’ relief.

Conditions for Claiming Investors’ Relief

There are certain requirements that must be met before an investor can be granted relief. Some of them are:

Issuance and Holding Period:

- Qualifying shares must be issued by the trading company on or after 17 March 2016.

- The shares must be held continuously for a minimum of three years.

Claim Deadline:

- A claim for relief must be submitted by the first anniversary of 31 January following the tax year in which the disposal takes place.

- For disposals in 2022/23, the claim deadline would be 31 January 2025.

Nature of Shares:

- Qualifying shares must be new ordinary shares acquired through individual cash subscriptions.

Unlisted Company:

- The company issuing the shares must have been unlisted at the time of share issuance.

Holding Size:

- There is no minimum or maximum requirement for shareholding size to be eligible for relief.

Relevant Employee Status:

- The relief is available only to individuals who are not considered ‘relevant employees.’

- ‘Relevant employees’ are defined as directors or employees of the company (or a connected company) during the three-year holding period.

Connected Individuals:

- Relief is denied if a person connected with the investor, is a relevant employee.

- However, relief remains available if such individual becomes an unremunerated director after the share purchase or an employee of the company 180 days after share issuance (without a reasonable prospect of becoming an employee at the time of share issuance).

When the original subscriber gives the shares they signed up for to their spouse, the spouse is considered to have signed up for the shares at the time they were first made available.

Sequence for claiming Relief

When a partial shareholding is sold, the task at hand is to determine the specific shares being sold. This is essential for calculating the proportion of the gain that qualifies for relief. To facilitate this determination, the legislation establishes a mechanism that dictates the order in which the shares are considered sold. This approach aims to maximise the relief applicable to both the current and future sales.

So, where part of a holding is sold, the legislation procedure prescribes the following order:

1st: Qualifying Shares

2nd: Excluded Shares

3rd: Potentially Qualifying Shares

Last in First Out

Let’s consider a scenario involving Max who invested in Horizon Enterprises, a trading company. The details are as follows:

Acquisition Details:

- On May 1, 2020, Max acquired 18,000 shares by subscribing for £18,000.

- On May 1, 2021, he subscribed an additional £27,000 to acquire 12,000 more shares.

- On May 1, 2022, Max purchased 9,000 shares for £36,000.

In total, he invested £81,000 to acquire 39,000 shares.

Sale Details:

On October 15, 2023, Max sold 20,000 shares for £120,000.

Important Points:

Max is not employed by Horizon Enterprises and falls into the higher rate tax bracket.

For the tax year 2023/24, this is Max’s only capital disposal.

Answer:

Let’s first understanding the types of shares:

- The 18,000 shares are Qualified Shares

- The 12,000 shares are Potentially Qualified Shares

- The 9,000 Shares are Excluded Shares

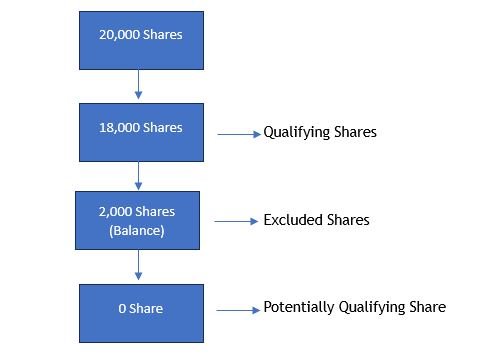

So, the 20,000 shares sold will be classified as:

Max will now deemed to have sold 18,000 qualifying shares, followed by 2,000 Excluded Shares.

The gain qualifying for Investors’ Relief will be 18,000/20,000

The gain on the disposal of the share is:

| Proceeds | £120,000 |

| Less: Cost (£81,000 x 20,000/39,000) | £41,538 |

| Gain | £78,462 |

| Gain Eligible for relief | Gain not eligible for relief | |

|---|---|---|

| Gain (£78,462 x 18,000/20,000) | 70,616 | |

| Gain (£78,462 x 2,000/20,000) | 7,846 | |

| Less: Annual Exempt Amount | (6,000) | |

| Taxable Gain | 70,616 | 1,846 |

| CGT: | ||

| 70,616 x 10% | 7,062 | |

| 1,846 x 20% | 369 | |

| 7,431 |

The remaining shares will be classified as follows:

- 10,000 are Excluded Shares

- 9,000 are Potentially Qualified shares

Investors’ Relief with EIS/SEIS Relief

An investment in shares within an unlisted trading company has the potential to meet the criteria for EIS/SEIS income tax relief, provided specific requirements are fulfilled. Under certain conditions, any gains from the sale of shares for which EIS/SEIS income tax relief was claimed could be free from Capital Gains Tax (CGT).

Therefore, a situation where claiming investors’ relief becomes pertinent is when the original share subscription did not qualify for income tax relief. This could be due to various reasons. For instance, the company might be engaged in a trade that doesn’t meet the criteria for EIS/SEIS relief, like property development.

Alternatively, the individual might have a connection with the company by holding over 30% of the ordinary shares, or the individual’s investment exceeding the maximum allowable limit for EIS/SEIS income tax relief within a given tax year.

Conclusion

In conclusion, investing in the financial market holds promise but also complexities, particularly in dealing with taxes. One avenue to ease this burden is “Investors’ Relief,” a tax advantage supporting investment in specific companies. This relief offers a 10% tax rate on gains from qualified share sales, with a lifetime cap of £10 million. It’s valuable when initial share subscriptions miss income tax relief qualifications.

Eligibility hinges on factors like share issuance, holding periods, unlisted company status, and employee connections. While this guide offers insights, consulting official sources or professionals for up-to-date information is vital. In the realm of investments and taxes, knowledge empowers smarter financial decisions.